Step 2 - Quantitative Analysis

Once we have the data, what will we do next?

Come up with an idea to serve as the backbone to a trading strategy!

2.1 Preparation Before the Action

Here are some packages and functions we will need later:

import matplotlib.pyplot as plt

import seaborn as sns

import numpy as np

import pandas as pd

from typing import Dict, List, Union, Optional, Any

import warnings

warnings.filterwarnings("ignore")

def plot_regressions(X, y, plots_in_col = 3, lowess=False):

labels = list(X.columns)

N, p = X.shape

rows = int(np.ceil(p/plots_in_col))

fig, axes = plt.subplots(rows, plots_in_col, figsize=(12, rows*(12/4)))

for i, ax in enumerate(fig.axes):

if i < p:

sns.regplot(X.iloc[:,i], y, ci=None, y_jitter=0.05,

scatter_kws={'s': 25, 'alpha':.8}, ax=ax, lowess=lowess,

line_kws={"color": "#c02c38"})

ax.set_xlabel('')

ax.set_ylabel('')

ax.set_title(labels[i])

else:

fig.delaxes(ax)

sns.despine()

plt.tight_layout()

plt.show()

return fig, axes

def plot_multiTS(data: pd.DataFrame, cols_idx: List, date_col: str):

sns.set_theme(style="darkgrid")

# cols_idx = [0, 1,3,4]

features = (len(cols_idx),1)

date = date_col

fig, axes = plt.subplots(features[0], features[1], figsize=(features[0]*4,10))

# data.date = pd.to_datetime(data.date)

for i in range(features[0]):

sns.lineplot(x = date,y = data.columns[cols_idx[i]], data = data,ax = axes[i,])

return fig

Next, we will read the data from the previous part.

data = pd.read_csv('../Data/btc_tg.csv', parse_dates=['DATE'])

2.2 Correlation Analysis

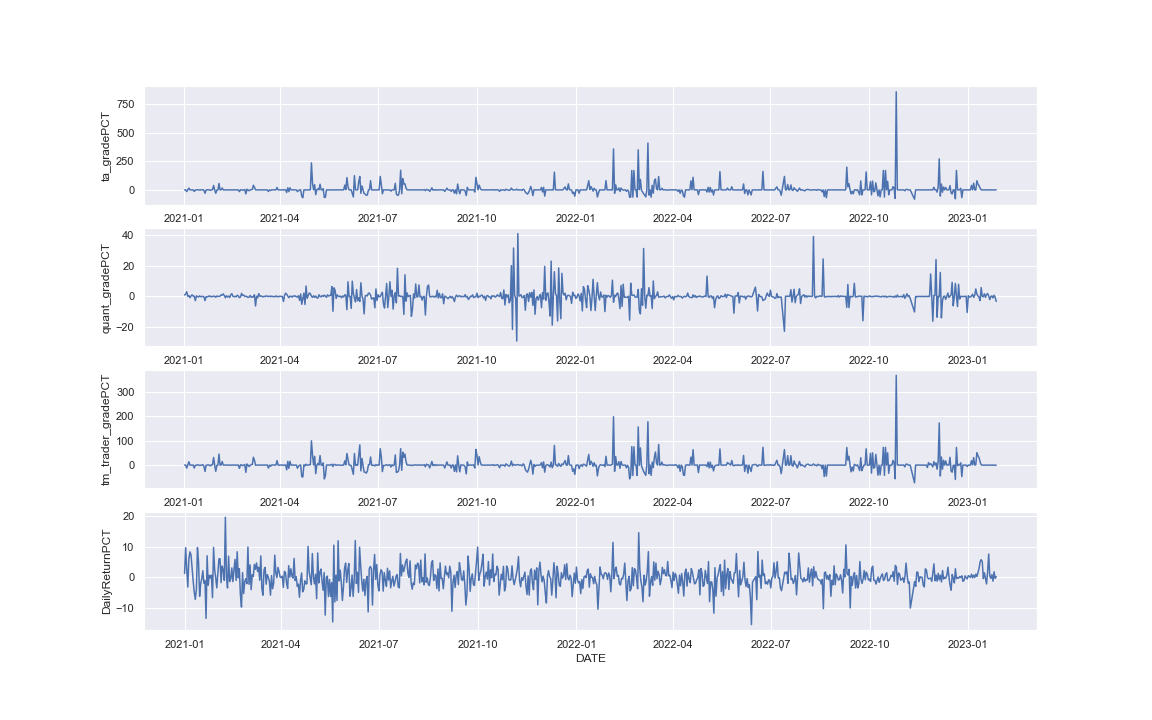

First, we should take a look at the relationship between those features.

fig = plot_multiTS(data[['TA_GRADE','QUANT_GRADE','TM_TRADER_GRADE','DailyReturnPCT','DATE']], list(range(4)), 'DATE')

From the plots above, we can observe the relationship:

- Both the

TM_TRADER_GRADEand theTA_GRADEhave similar features. - There seems to be a high relationship between the

TA_GRADEand theDailyReturnPCT. For example, when we were looking at the high volatility part of theDailyReturnPCT, it is clear that bothTM_TRADER_GRADEandTA_GRADEwere encountering volatility as well. QUANT_GRADEcontributes little to theDailyReturnPCT.

Let's move further, doing some transformation and statistics.

fig = plot_multiTS(data[['ta_gradePCT','quant_gradePCT','tm_trader_gradePCT','DailyReturnPCT','DATE']], list(range(4)), 'DATE')

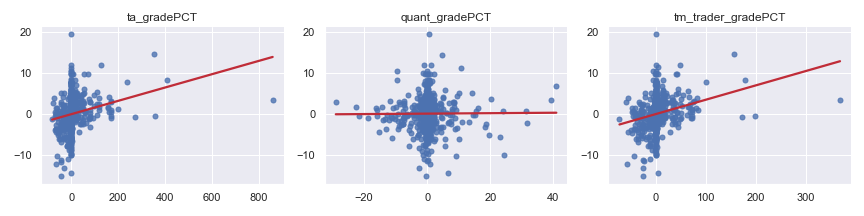

Now, let's do simple linear regression to verify this relationship.

fig,axes = plot_regressions(data[['ta_gradePCT','quant_gradePCT','tm_trader_gradePCT']], data['DailyReturnPCT'], plots_in_col = 3)

Here we can observe two positive relationships:

ta_gradePCTvs.DailyReturnPCTtm_trader_gradePCTvs.DailyReturnPCT

Fill null data and save the data for later.

# Handle missing values

data = data.fillna(method='ffill')

data[['DATE','Open','High','Low','Close','Volume','TA_GRADE','QUANT_GRADE','TM_TRADER_GRADE']].sort_values(by = 'DATE').to_csv('../Data/TMdata.csv', index=False)

2.3 Coming up with a Trading Idea

We saw strong and positive relationships for both TA_GRADE, TM_TRADER_GRADE with DailyReturnPCT. Let me give an example to explain the positive relationship and how we can derive a trading idea:

What we have:

-

DailyReturnPCT= TheClose priceof the day - theOpen priceof the day. -

Our

TM_TRADER_GRADEwill be updated at start of the day. -

There is a significant positive relationship between the

DailyReturnPCTandTM_TRADER_GRADE.

Here is the scenario:

Now it is the Morning of 01/27/2023I received today's TM_TRADER_GRADE of Bitcoin and it shows an upward trend, so I purchasedBitcoin and waited for the day to end.

When it comes to the end of the day of 01/27/2023I sold my Bitcoin position and obtained a 0.1% profit over the day.

What we will do:

Based on the above scenario, let's move it into a more professional description and come up with the following trading logic:

- Feature:

TM_TRADER_GRADE - Trading pair:

BTCUSDT Perpetual - Exchange:

Binance US - Buy signal: When the

TM_TRADER_GRADEshows an up-trend - Sell signal: When the

TM_TRADER_GRADEshows a down-trend - Position:

Long,Short - Commission fee:

0.04% - Size:

All in - Starting Cash:

$100,000 - Price slippage:

Almost ignorable(24h Volume (USDT) forBTCUSDT Perpetual:$17B) - Frequency:

Daily - When entering the market:

00:00:00 - When out of the market:

23:59:59

Once we develop this exciting trading strategy, professional backtesting is necessary to verify and measure the design. This is what we will cover in Step 3.

Updated 10 days ago