Step 3 - Backtesting and Analysis

Open the recipe for a walk-through on how to code this

Recall from the previous step, here is what we defined about the signal:

-

Buy signal: When the

TM_TRADER_GRADEshows an up-trend -

Sell signal: When the

TM_TRADER_GRADEshows a down-trend

EMA could be one of the notable ways to follow the trend. Therefore, we represent our signals in mathematical ways

-

Buy Signal: When the

EMA(3)of theTM_TRADER_GRADE>=EMA(7)of theTM_TRADER_GRADE -

Sell Signal: When the

EMA(3)of theTM_TRADER_GRADE<EMA(7)of theTM_TRADER_GRADE

A professional and comprehensive backtesting framework must be grasped if you want to act as a professional quantitative trader. Please refer to [Simple Backtesting](##Simple Backtesting) for people with a limited background in backtesting. If you are a professional quantitative trader, please refer to the [Advanced Backtesting](##Advanced Backtesting).

3.1 Simple Backtesting

3.1.1 Backtesting

To implement a simple backtesting process, we first calculated the daily return and our signal (True: Buy Signal, False: Sell Signal).

Then, for each day, we calculate the daily portfolio return.

For example, given

2021-01-01, we received theTrueSignal at the start of the day, then, we will assume we earnDailyReturnPCT,1.2837%for that day.

import pandas as pd

# Read data

data = pd.read_csv('data/TMdata.csv', index_col=0, parse_dates=True)

# Calculate daily return and Signal

data['DailyReturnPCT'] = data['Close']/data['Open']-1

data['EMA_TraderGrade_Fastline'] = data['DailyReturnPCT'].ewm(span=3).mean()

data['EMA_TraderGrade_Slowline'] = data['DailyReturnPCT'].ewm(span=7).mean()

data['Signal'] = data['EMA_TraderGrade_Fastline'] >= data['EMA_TraderGrade_Slowline']

# Calculate portfolio return

data['PortfolioReturnPCT'] = data.apply(lambda x: x['DailyReturnPCT'] if x['Signal'] else -x['DailyReturnPCT'], axis=1)

| DATE | Open | High | Low | Close | Volume | TA_GRADE | QUANT_GRADE | TM_TRADER_GRADE | DailyReturnPCT | EMA_TraderGrade_Fastline | EMA_TraderGrade_Slowline | Signal | PortfolioReturnPCT | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2021-01-01 | 28933.86 | 29611.51 | 28649.46 | 29305.29 | 298.357085 | 95.941921 | 52.077850 | 87.169107 | 1.283721 | 87.169107 | 87.169107 | True | 1.283721 |

| 1 | 2021-01-02 | 29321.41 | 33271.38 | 28955.02 | 32162.01 | 667.482338 | 96.085594 | 52.550240 | 87.378523 | 9.687802 | 87.308718 | 87.288773 | True | 9.687802 |

| 2 | 2021-01-03 | 32174.75 | 34776.59 | 31942.96 | 33031.74 | 701.951087 | 96.124244 | 53.365372 | 87.572470 | 2.663548 | 87.459433 | 87.411453 | True | 2.663548 |

| 3 | 2021-01-04 | 33034.55 | 33593.47 | 27500.00 | 32005.27 | 987.279894 | 82.142057 | 54.996140 | 76.712873 | -3.115768 | 81.727934 | 83.498829 | False | 3.115768 |

3.1.2 Analysis

Here is our approximate backtesting result

- The average daily return will be

0.6014%, or24.54%annual return rate.

data['PortfolioReturnPCT'].mean()

# 0.6014

The compound annual return calculation: (1+0.0006014)^365 - 1 = 0.2454

- The total return will be

449.22%

data['PortfolioReturnPCT'].sum()

# 449.22

Amazing! We successfully built a profitable trading strategy!

However, we should admit that the simple backtesting process was inaccurate because it ignored many factors, for example, the commission fee. Please move to the next section if you want an accurate backtesting result.

3.2 Advanced Backtesting

3.2.1 Building Signal

We introduced a professional backtesting framework to simulate live trading: Backtrader.

Here is the main logic for the strategy:

class EMACloseSignal(bt.Indicator):

lines = ('trader_grade_A', 'trader_grade_B', 'signal')

params = (('period_A', None),('period_B', None),)

def __init__(self):

self.lines.trader_grade_A = bt.talib.EMA(self.datas[0].trader_grade, timeperiod=self.p.period_A, subplot=True)

self.lines.trader_grade_B = bt.talib.EMA(self.datas[0].trader_grade, timeperiod=self.p.period_B, subplot=True)

self.lines.signal = self.lines.trader_grade_A > self.lines.trader_grade_B

We defined the rule:

When the faster EMA line, trader_grade_A, of the trader grade crosses over the slower EMA line, trader_grade_B, we should be in the Long position. Otherwise, we should hold the Short position.

3.2.2 Building Trading Logic

Here is the Long-Short strategy

def next(self):

# ......

# We are not in the market

if not self.position:

if self.signal[0]: # Buy signal

self.log(f"BUY CREATE, {self.dataclose[0]}")

self.order = self.buy(size=size) # Long position

else: # Sell signal

self.log(f"SELL CREATE, {self.dataclose[0]}")

self.order = self.sell(size=size) # Short position

# We in a short position but given a Buy signal

elif self.signal[0] and self.position.size < 0:

self.log(f"SELL Close, {self.dataclose[0]}")

self.order = self.close() # we close our current position

# We in a long position but given a Sell signal

elif not self.signal[0] and self.position.size > 0:

self.log(f"BUY Close, {self.dataclose[0]}")

self.order = self.close()

Here is the explanation for the above code:

if we do not hold position:

if it is a buy signal:

we buy!!! --> Long position

else it is a sell signal:

we sell!!! --> Short position

else if the signal is buy but we hold the short position :

we closed our short position

else if the signal is sell but we hold the long position:

we closed our long position

It is straightforward, right? Let's run it and see our potential ROI with the strategy.

3.2.3 Backtesting parameter

Before we start our backtesting, we still need to set some parameters to simulate a live trading environment.

Starting cash will be set with $100,000

cerebro.broker.setcash(100000.0)

The commission will be set with 0.04% referred to as the USD-M Futures Trading - USDT Maker/Taker from Binance

cerebro.broker.setcommission(commission=0.0004)

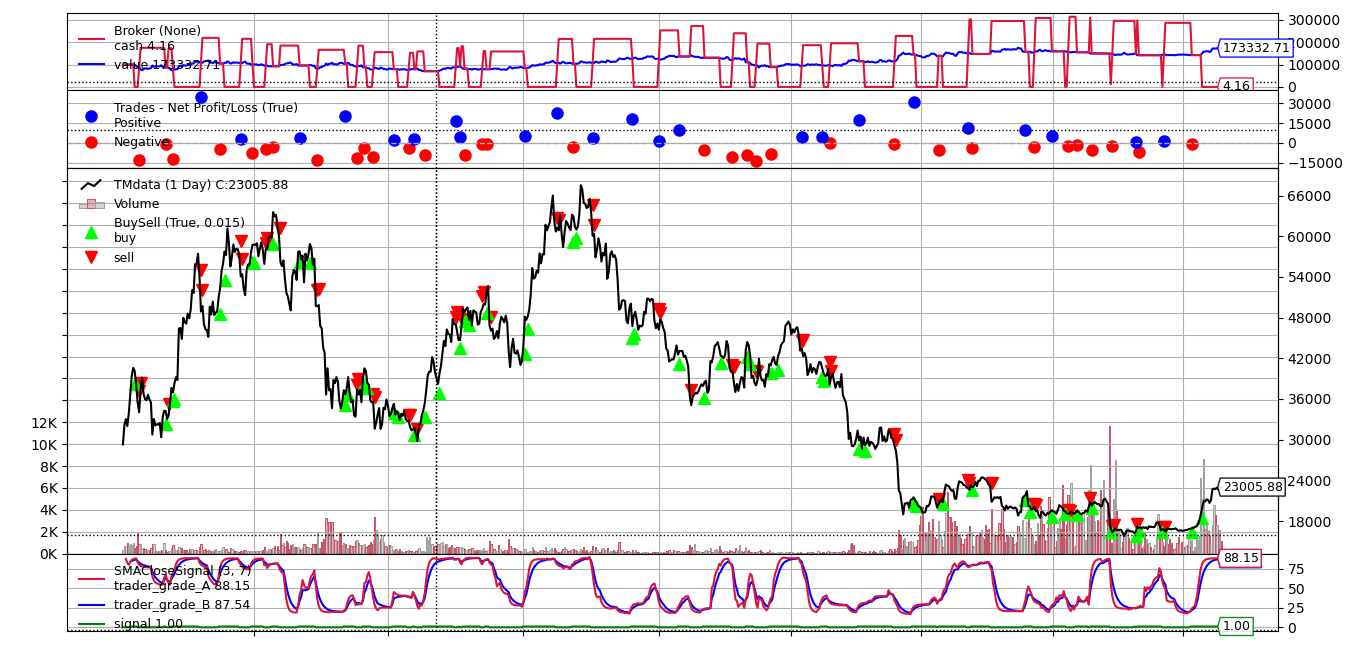

3.2.4 Analysis

Wow, pretty good! Our capital increased from $100,000 to $173,332.71 over nearly two years.

Starting Portfolio Value: 100000.00

Final Portfolio Value: 173332.71

Sharpe Ratio: 4.084129867662106

DrawDown: 40.249658800933624

Sharpe Ratio reached almost 4.1!

Now that we can say this trading strategy works, what will be next?

We just need to implement it in our real account and prepare to watch the ROI move!

Appendix

Backtesting.py

import backtrader as bt

import backtrader.feeds as btfeeds

class TM_API_data(btfeeds.GenericCSVData):

# add only three columns called date, Bitcoin, Ethereum

lines = ('ta_grade','quant_grade','trader_grade')

params = (

('nullvalue', float('NaN')),

('dtformat', '%Y-%m-%d'),

# ('tmformat', '%H:%M:%S'),

('datetime', 0),

# ('time', 0),

('open', 1),

('high', 2),

('low', 3),

('close', 4),

('volume', 5),

('openinterest', -1),

('ta_grade', 6),

('quant_grade', 7),

('trader_grade', 8),

)

class EMACloseSignal(bt.Indicator):

lines = ('trader_grade_A', 'trader_grade_B', 'signal')

params = (('period_A', None),('period_B', None),)

def __init__(self):

self.lines.trader_grade_A = bt.talib.EMA(self.datas[0].trader_grade, timeperiod=self.p.period_A, subplot=True)

self.lines.trader_grade_B = bt.talib.EMA(self.datas[0].trader_grade, timeperiod=self.p.period_B, subplot=True)

self.lines.signal = self.lines.trader_grade_A > self.lines.trader_grade_B

class TMStrategy(bt.Strategy):

params = (('period_A', None),('period_B', None),)

def log(self, txt, dt=None):

''' Logging function for this strategy'''

dt = dt or self.datas[0].datetime.date(0)

# print('%s, %s' % (dt, txt))

def __init__(self):

"""Initialize the strategy"""

self.dataclose = self.datas[0].close

# for single strategy

self.myindicator = EMACloseSignal(self.datas[0], period_A=self.p.period_A, period_B=self.p.period_B, plot=True)

self.signal = self.myindicator.lines.signal

# To keep track of pending orders

self.order = None

self.buyprice = None

self.buycomm = None

def calculate_size(self,slipage = 0.1):

# full position

cash = self.broker.get_cash()

size = cash/(self.data.close[0] * (1+slipage))

return size

def next(self):

"""Run once per data bar"""

size = self.calculate_size(slipage=0)

self.log(f"Close, {self.dataclose[0]}, ta_grade, {self.datas[0].trader_grade[0]}, signal, {self.signal[0]}, tg_A, {self.myindicator.lines.trader_grade_A[0]}, tg_B, {self.myindicator.lines.trader_grade_B[0]}")

# Check if an order is pending

if self.order:

return

# We are not in the market

if not self.position:

if self.signal[0]: # Buy signal

self.log(f"BUY CREATE, {self.dataclose[0]}")

self.order = self.buy(size=size) # Long position

else: # Sell signal

self.log(f"SELL CREATE, {self.dataclose[0]}")

self.order = self.sell(size=size) # Short position

# We in a short position but given a Buy signal

elif self.signal[0] and self.position.size < 0:

self.log(f"SELL Close, {self.dataclose[0]}")

self.order = self.close() # we close our current position

# We in a long position but given a Sell signal

elif not self.signal[0] and self.position.size > 0:

self.log(f"BUY Close, {self.dataclose[0]}")

self.order = self.close()

def notify_order(self, order):

if order.status in [order.Submitted, order.Accepted]:

# Buy/Sell order submitted/accepted to/by broker - Nothing to do

return

# Check if an order has been completed

# Attention: broker could reject order if not enough cash

if order.status in [order.Completed]:

if order.isbuy():

self.log(

'BUY EXECUTED, Price: %.2f, Cost: %.2f, Comm %.2f' %

(order.executed.price,

order.executed.value,

order.executed.comm))

self.buyprice = order.executed.price

self.buycomm = order.executed.comm

elif order.issell() : # Sell

self.log('SELL EXECUTED, Price: %.2f, Cost: %.2f, Comm %.2f' %

(order.executed.price,

order.executed.value,

order.executed.comm))

elif order.isclose():

self.log('Order closed EXECUTED, Price: %.2f, Cost: %.2f, Comm %.2f' %

(order.executed.price,

order.executed.value,

order.executed.comm))

self.bar_executed = len(self)

elif order.status in [order.Canceled, order.Margin, order.Rejected]:

self.log('Order Canceled/Margin/Rejected')

# Write down: no pending order

self.order = None

def notify_trade(self, trade):

if not trade.isclosed:

return

self.log('OPERATION PROFIT, GROSS %.2f, NET %.2f' %

(trade.pnl, trade.pnlcomm))

def runstart():

cerebro = bt.Cerebro(cheat_on_open=True)

cerebro.addstrategy(TMStrategy, period_A=3, period_B=7)

# cerebro.optstrategy(TMStrategy, period_A=range(2, 10), period_B=range(2, 10))

cerebro.addanalyzer(bt.analyzers.PyFolio, _name='pyfolio')

cerebro.addanalyzer(bt.analyzers.SharpeRatio, _name='SharpeRatio')

cerebro.addanalyzer(bt.analyzers.Returns, _name='Returns')

cerebro.addanalyzer(bt.analyzers.DrawDown, _name='DrawDown')

cerebro.broker.setcash(100000.0)

cerebro.adddata(TM_API_data(dataname='data/TMdata.csv'))

cerebro.broker.setcommission(commission=0.0004)

print('Starting Portfolio Value: %.2f' % cerebro.broker.getvalue())

result = cerebro.run()

print('Final Portfolio Value: %.2f' % cerebro.broker.getvalue())

# # for optimization

# for strat in result:

# print('Parameters:', strat[0].p.period_A, strat[0].p.period_B)

# print('Sharpe Ratio:', strat[0].analyzers.SharpeRatio.get_analysis()['sharperatio'])

# print('Returns:', strat[0].analyzers.Returns.get_analysis()['rtot'])

# for single strategy

strat = result[0]

print('Sharpe Ratio:', strat.analyzers.SharpeRatio.get_analysis()['sharperatio'])

print('Returns:', strat.analyzers.Returns.get_analysis()['rtot'])

print('DrawDown:', strat.analyzers.DrawDown.get_analysis()['max']['drawdown'])

# pyfoliozer

pyfoliozer = strat.analyzers.getbyname('pyfolio')

returns, positions, transactions, gross_lev = pyfoliozer.get_pf_items()

returns.to_csv('result/returns.csv')

positions.to_csv('result/positions.csv')

transactions.to_csv('result/transactions.csv')

gross_lev.to_csv('result/gross_lev.csv')

cerebro.plot()

if __name__ == '__main__':

runstart()

Updated 6 months ago